Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

When Hurricane Helene tore through western North Carolina in the fall of 2024, the damage was immense—washed-out roads, flooded valleys, homes destroyed from the mountains to the Piedmont. But beyond the wreckage, something else changed: the way North Carolinians think about property, safety, and value.

A year later, that storm continues to ripple through the state’s real estate market. Buyers are asking new questions, sellers are rethinking how they market homes, and agents are finding that conversations about climate risk are becoming as essential as discussions about price, school districts, or upgrades.

This post explores how climate concerns—rising insurance costs, updated flood data, and evolving city planning—are transforming housing decisions across North Carolina, and what it means for those of us working in real estate today.

The Wake-Up Call After Helene

For decades, North Carolina’s real estate conversations were dominated by familiar themes: square footage, neighborhoods, schools, and commute times. Flood maps and stormwater design rarely made the list. That changed after Helene.

The storm’s flooding extended far beyond designated FEMA flood zones. Homeowners who had never worried about water damage suddenly found themselves dealing with ruined basements and insurance claims. For many, it was the first time they realized that official flood maps often underestimate risk.

As one Triangle-area agent observed, clients now routinely ask about flood history, drainage, and stormwater management before they even schedule a showing. Buyers who once relied solely on FEMA maps are discovering new tools—such as the First Street Foundation’s “ClimateCheck” scores on Zillow—that predict how flood, heat, or wildfire risks might evolve in the decades ahead.

This shift has created both greater awareness and greater uncertainty. Some homebuyers are finding that different tools produce conflicting results: a FEMA map may show no risk, while a private data model labels the same property as high-risk. Agents increasingly find themselves acting as interpreters, helping clients make sense of the numbers.

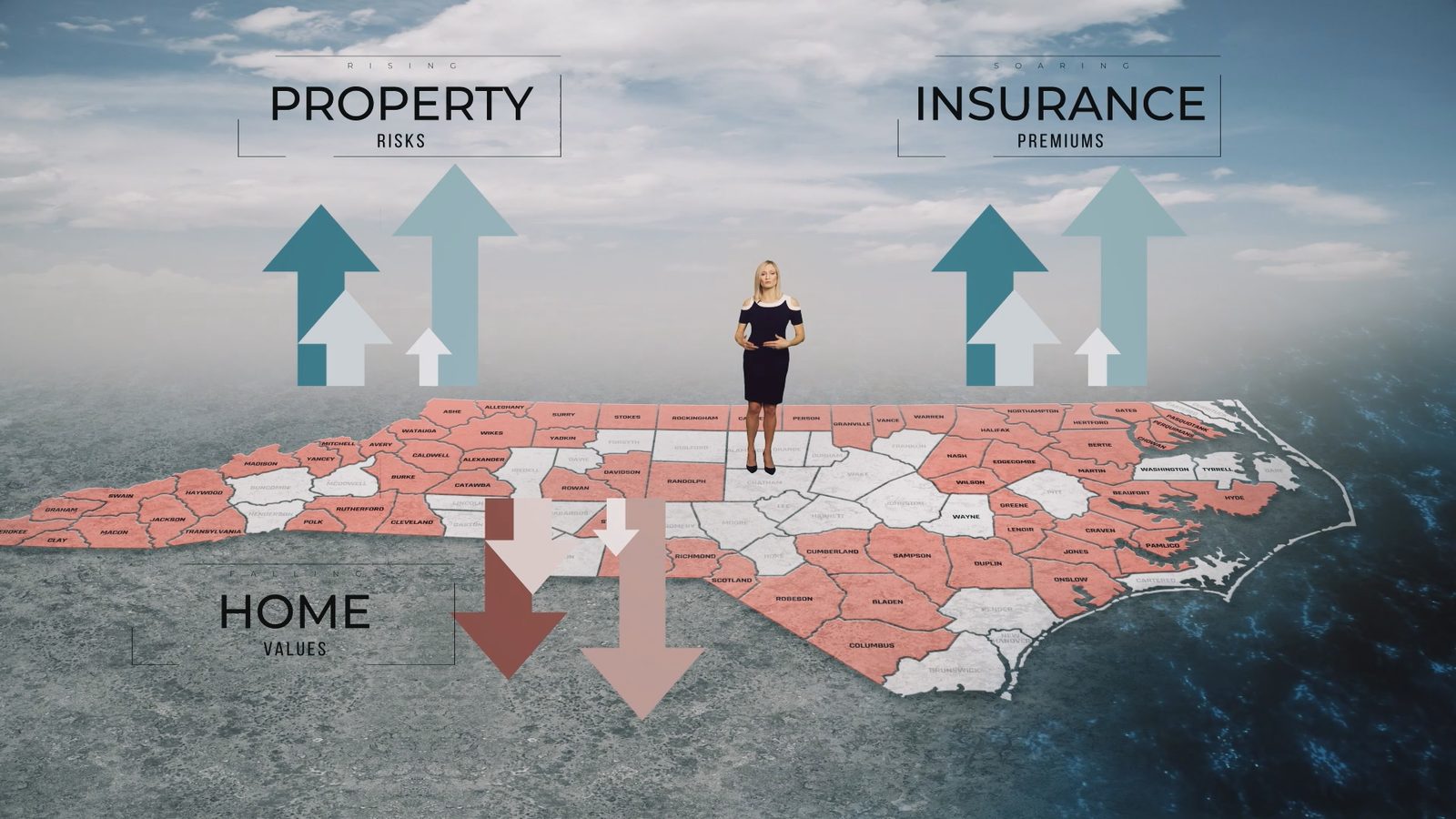

The Insurance Squeeze

The financial side of climate risk is also getting harder to ignore. Home insurance premiums have been rising across the country, but in North Carolina the increases have been especially steep. The state’s Department of Insurance has received requests from major carriers seeking double-digit rate hikes, and in some coastal counties, proposed increases approach 100 percent.

These changes are driven by a simple equation: more extreme weather equals more claims. Even inland counties, far from the ocean, have seen insurers tighten coverage after repeated flooding and storm damage. Some national insurance companies have already scaled back their presence in the state, leaving smaller regional carriers to fill the gap.

For buyers, this means the “monthly payment” conversation now includes more than principal and interest. Insurance can add hundreds of dollars per month—sometimes making an otherwise affordable home out of reach. For sellers, that can limit the buyer pool.

What used to be a background cost is now a central factor in affordability, and savvy realtors are learning to address it early in the process rather than leaving it as an unwelcome surprise at closing.

New Tools, New Data, and New Responsibilities

For decades, FEMA’s official floodplain maps were the standard reference for understanding property risk. But as weather patterns change and rainfall intensity increases, local governments and private researchers have begun producing far more detailed and forward-looking maps.

The First Street Foundation, a nonprofit research group, now offers property-level flood and wildfire risk data used by Zillow, Redfin, and Realtor.com. These predictive models take into account future rainfall projections, elevation, and climate trends, not just historical flood events.

That can lead to uncomfortable contradictions. A home that appears outside FEMA’s “high risk” zone might still have a one-in-five chance of flooding during the life of a 30-year mortgage. In a post-Helene market, those discrepancies are shaping buyer behavior.

Real estate professionals are adapting quickly. Many agents are developing relationships with local stormwater divisions or floodplain managers who can provide parcel-specific data for their clients. Others are learning to translate complex risk scores into plain-language advice: what it means for insurance, for resale value, and for peace of mind.

For many in the industry, this represents an ethical shift as much as a practical one. Helping clients navigate climate information is no longer a niche skill—it’s part of fiduciary duty.

How Buyers Are Changing

Despite rising awareness, most homebuyers in North Carolina still begin their search the same way: with a budget and a preferred area. Climate concerns usually enter the conversation later, often when insurance quotes or inspection results reveal hidden risks.

But that pattern is evolving. Younger buyers, especially first-timers, are increasingly cautious about long-term vulnerability. Many are asking whether their investment will hold value if flooding becomes more frequent or if insurance costs keep rising.

In coastal and mountain communities alike, buyers are weighing elevation, drainage, and municipal flood-mitigation plans in ways that were once reserved for waterfront properties. Even in fast-growing suburbs around Raleigh, Clayton, and Johnston County, stormwater infrastructure and floodplain boundaries are now part of the due-diligence checklist.

That doesn’t mean most people are avoiding high-risk areas entirely—price and location still drive most decisions—but climate awareness is quietly reshaping how those trade-offs are made.

Developers and Builders Feel the Pressure

The development community is facing its own reckoning. Cities like Raleigh and Wilmington are revising their long-term plans to integrate climate resilience directly into growth policy. That means stricter stormwater standards, incentives for preserving tree canopy, and, in some cases, zoning changes that favor denser, more vertical building over horizontal sprawl.

As heavy rainfall events become more common, low-lying neighborhoods that once seemed safe are now experiencing nuisance flooding. Planners and developers are responding with new building codes, raised foundations, and permeable materials that help reduce runoff.

In practice, this means builders who adopt resilient design are gaining a competitive edge. Features like elevated crawlspaces, reinforced drainage systems, and native landscaping that handles heavy rain aren’t just environmentally responsible—they’re marketable.

As one industry leader put it, resilience is fast becoming a selling point in its own right, much like energy efficiency or smart-home technology was a decade ago.

The Expanding Role of Realtors

For realtors, this changing landscape presents both a challenge and an opportunity. The challenge lies in mastering new kinds of information—flood data, insurance trends, local infrastructure plans—and communicating it clearly to clients.

The opportunity lies in becoming a trusted guide through uncertainty. When buyers confront conflicting maps or hear alarming news about climate risks, they need context. A well-informed agent can help them balance risk and reward, understand mitigation options, and make confident decisions.

Practically, this means adding a few new habits to the toolkit:

-

Check multiple sources. Don’t rely on FEMA maps alone. Compare with First Street Foundation data, city floodplain maps, and insurance disclosures.

-

Talk about insurance early. Buyers appreciate transparency about premiums, deductibles, and coverage limits.

-

Highlight resilience features. If a property has updated drainage, a newer roof, or sits on higher ground, emphasize that.

-

Build relationships with local experts. Stormwater engineers, insurance agents, and home inspectors who specialize in moisture management can become invaluable partners.

-

Educate your clients. Treat climate literacy as part of your service—just like explaining financing or market comps.

The goal isn’t to scare people away from certain areas. It’s to help them understand what they’re buying and how to protect it.

Sellers and Investors Must Adjust, Too

Sellers who have made resilience improvements—like installing sump pumps, adding French drains, or elevating utilities—should document those upgrades and include them in their marketing. A well-maintained property that demonstrates proactive risk management can stand out even in a competitive market.

Investors, meanwhile, are rethinking portfolio strategy. Properties in flood-prone or storm-exposed zones may face rising insurance costs, lower rentability, or slower appreciation. On the flip side, homes in resilient or elevated neighborhoods could see stronger long-term demand.

Market segmentation is likely to grow: buyers will pay premiums for perceived safety, while risky zones could experience flat or declining values. For landlords, this may translate to higher operating costs and tighter margins, reinforcing the importance of geographic diversification.

A Shift in Urban Form

As climate patterns change, cities are reimagining how they grow. Raleigh’s comprehensive plan for the next 20 years, for instance, emphasizes building “up rather than out” to preserve open space, protect tree canopy, and limit stormwater runoff.

This approach may sound abstract, but it’s already visible in zoning revisions that allow taller multifamily housing near transit corridors and require better stormwater systems for new subdivisions. By encouraging density in strategic areas, municipalities hope to reduce development pressure in flood-sensitive zones.

For real estate professionals, these shifts will affect everything from lot values to permitting timelines. Staying informed about local planning updates can help you anticipate where infrastructure investment—and buyer demand—will flow next.

What It Means for North Carolina’s Housing Market

The impact of climate awareness isn’t just philosophical—it’s financial. Across the state, climate risk is becoming part of how properties are valued.

-

Insurance costs are influencing affordability. Buyers calculate not only mortgage payments but also coverage premiums and deductibles.

-

Flood resilience is part of perceived value. Homes on higher ground or with modern drainage command stronger offers.

-

Data transparency is shaping demand. With risk scores visible on listing sites, buyers have more information—but also more questions.

-

Development patterns are evolving. Municipalities are emphasizing stormwater management and compact growth.

-

Buyer psychology is shifting. Especially among younger generations, there’s a growing sense that sustainability and stability go hand in hand.

In short, resilience is emerging as both an ethical and economic driver of the housing market.

A Parallel from the Mountains

As someone who rock climbs, I can’t help noticing the parallels. When you plan a climb, you study the route, check the forecast, and prepare for changing conditions. Real estate now demands the same mindset.

Just as a climber weighs risk exposure before committing to a wall, today’s buyers are learning to assess exposure to flooding, heat, and wind before committing to a home. And just as the best climbers respect the mountain rather than deny its challenges, the best property professionals acknowledge climate realities and prepare their clients accordingly.

That approach doesn’t make real estate less hopeful—it makes it more resilient.

Looking Ahead

Over the next decade, expect climate awareness to become a standard part of homeownership in North Carolina. Insurers, lenders, and municipal governments are already adjusting their models. Buyers will follow.

For realtors, that means opportunity: the chance to lead with knowledge, to guide clients through a changing landscape, and to position resilience as a hallmark of good investment.

The homes we sell today will weather the storms of the next generation. Helping clients choose wisely—balancing location, affordability, and resilience—will define what it means to be an expert in this new era of North Carolina real estate.